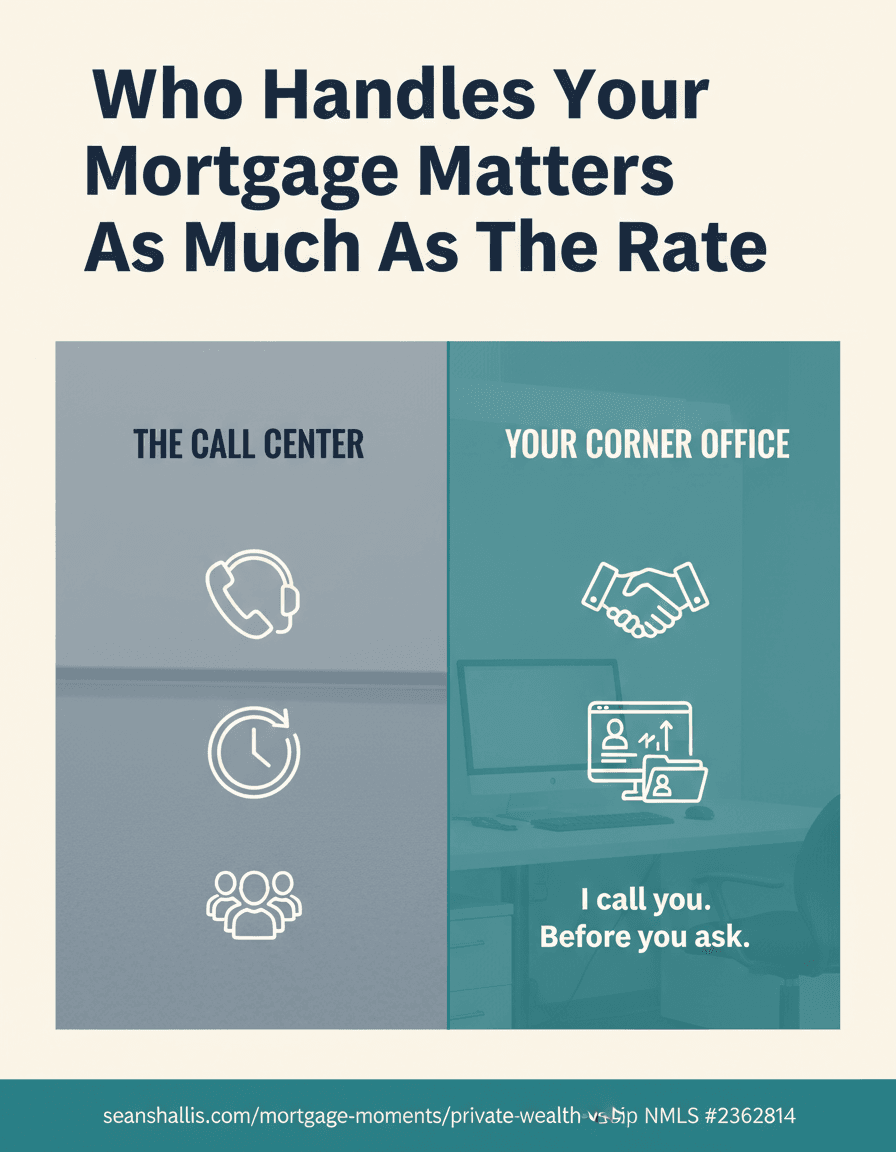

The Call Center vs. Your Corner Office

A client got a lower rate from a big bank. Here's what they didn't get — and why the person on the other end of that phone has no stake in whether your deal actually closes.

A Message I Received This Week

“We're going in a different direction. A big bank called us and offered a rate with a relationship discount. Hope you understand — it was too good for us to pass up. We'll share your contact with our network.”

I get messages like this a few times a year. And I always respond the same way: I genuinely wish them well — and I share one piece of advice they didn't ask for, because it's the one that could save the deal.

The rate is real. The risk usually isn't in the rate sheet. It's in what happens when something goes sideways — and the person on the other end of the phone has already moved on to the next file.

The Number vs. The Deal

Big banks offer rates. That's what they do well. They have marketing budgets, brand recognition, and pricing power that comes from volume. When a large institution dangles a relationship discount, it can feel like preferential treatment — like someone on the inside went to bat for you.

But here's what most buyers don't realize until it's too late: the person who quoted you that rate is working a queue. They have dozens of files open simultaneously. They didn't analyze your specific property, your specific loan type, or the nuances of your transaction. They ran a scenario through a pricing engine and delivered a number.

A number is not a deal. A deal is what happens between application and closing — and a lot can happen in between.

Skin in the Game

When I take on a client, my name goes on the file. My reputation is attached to the outcome. If your deal falls apart, I lose sleep — not just the commission. I have one version of success: you close, you're happy, and the numbers did what I told you they would do.

A call center rep at a big institution doesn't have that exposure. If your deal doesn't close, they move to the next one in the queue. There's no relationship at stake. No referral network built on the outcome. No long-term accountability to you as a client.

That's not a criticism of the individual. It's a structural reality. Large banks are built for volume and efficiency — not for the kind of deal-level advocacy that complex transactions require.

- —Competitive rates from volume pricing

- —Call center queue — your file is one of dozens

- —Rep has no stake in your closing outcome

- —Rate quoted; deal managed by whoever picks up

- —Escalation is a ticket number, not a phone call

- —If it falls apart, they move to the next file

- ✓Competitive rates with full program access

- ✓One point of contact — start to close

- ✓Reputation and referral network on the line

- ✓Deal reviewed at the property and loan level

- ✓Escalation is a direct call, same day

- ✓Your outcome is their outcome — period

The Warning I Always Give

When a client tells me they're going with a large institution — especially on a Jumbo or non-conforming loan — I always share one piece of unsolicited advice: make sure the property appraises before you cancel your existing approval.

Large banks often use in-house or captive appraisal panels that skew conservative — particularly on higher-end properties where comparable sales are thin. If the appraisal comes in low, the deal can implode. And the call center rep who quoted you the rate cannot walk the appraiser through the comps, appeal the value, or fight for the file the way someone who has been in this market for 30 years can.

This isn't fear-mongering. It's the kind of thing a trusted advisor tells you — not because they want your business back, but because it's the right thing to say.

What You're Actually Buying

When you work with a private wealth mortgage strategist, you're not just buying a rate. You're buying access to someone who:

Picks up the phone

Not a ticket system. Not a callback queue. When something happens on your deal — an appraisal issue, a condition, a rate lock expiration — you call and someone who knows your file answers.

Knows your transaction at the deal level

Your property type, your income structure, your timeline, your goals. Not a generic scenario run through a pricing engine — your actual deal, reviewed by someone who has closed hundreds like it.

Tells you what can go wrong before it does

A good advisor surfaces risk before it becomes a problem. Appraisal exposure, rate lock timing, debt-to-income nuances — these are the conversations that protect you, and they only happen when someone is actually paying attention.

The Bottom Line

If a large bank's rate is genuinely lower and the transaction is straightforward — conventional loan, clean income, standard property — the math might work in their favor. I'll tell you that honestly.

But if your deal has any complexity — a Jumbo balance, a non-warrantable property, a self-employed income structure, a tight timeline — the person fielding your file matters as much as the rate on the term sheet. Maybe more.

A rate is a starting point. A trusted advisor is the thing that gets you to the closing table when it matters most. Make sure you know which one you're actually getting.

Mortgage Moments

Want a second opinion before you commit?

If you've been quoted a rate and want to know whether it's actually the best move for your specific deal, ask Rosie for a free check — or book a call and let's walk through it together.

Sean Shallis · Mortgage Loan Originator · NMLS #2362814. This post is for educational purposes only and does not constitute financial or mortgage advice. All comparisons are general in nature. Individual loan outcomes depend on credit, property, income, loan program, and lender. Contact Sean for a personalized analysis of your specific situation. Equal Housing Lender.