One Close. One Expert. Zero Surprises.

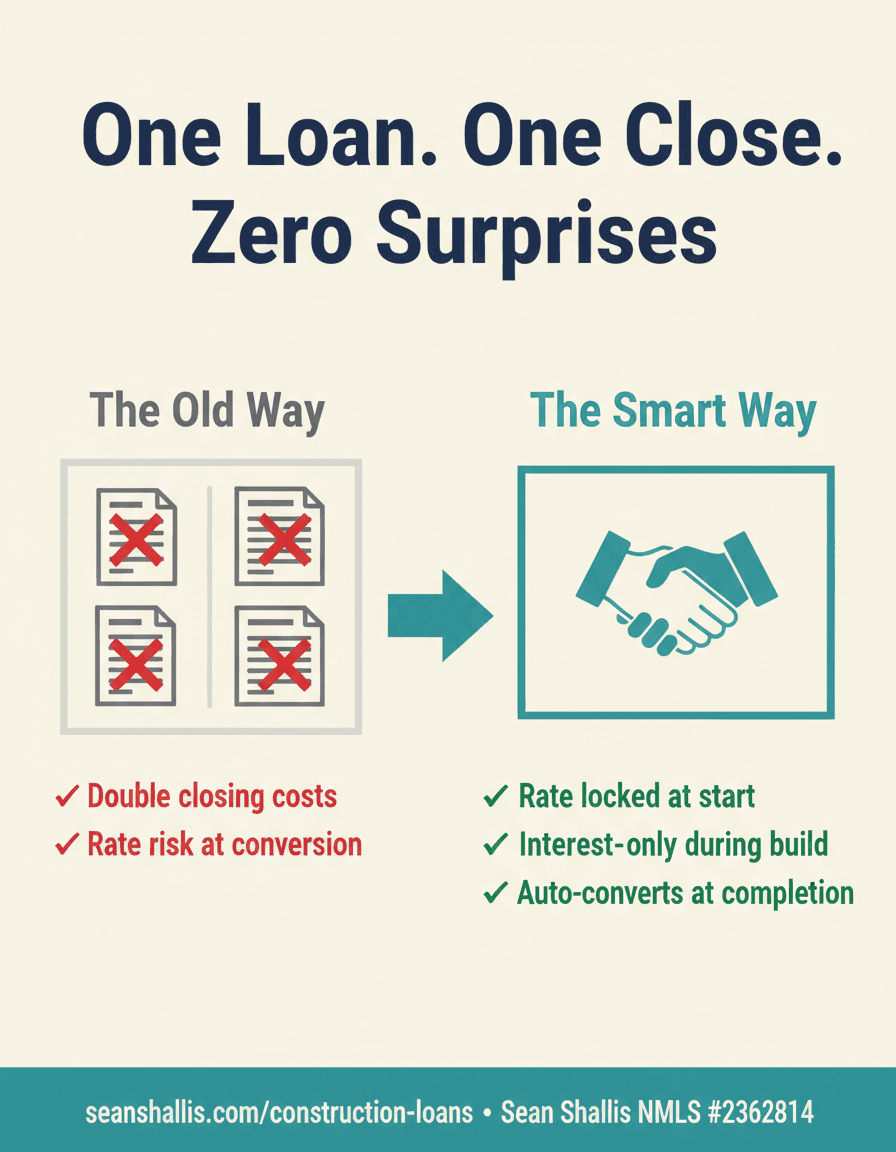

Construction-to-permanent financing that combines your build loan and mortgage into a single close. No double closing costs. Interest-only during construction. Sean manages the draw schedule so you can focus on the build.

Who this is for.

Whether you're building from scratch, gutting a fixer, or combining physician benefits with construction financing — Sean structures the loan so you can focus on the build.

Custom Build

Building your dream home from the ground up. One loan, one close, one rate lock from dirt to doorstep.

Major Renovation

Gut renos and renovation-to-permanent projects. Transform an existing structure without juggling multiple loans.

Physician Builders

Physicians building custom homes can combine construction-to-perm with physician loan benefits. Zero down available.

Investment Builders

Developers building rental or flip properties. Competitive terms for experienced investors with $100K+ projects.

Numbers that make the build make sense.

Single close saves $5-15K vs. two-close construction loans

Pay only interest on funds drawn — not the full loan amount

Lock your permanent rate before construction begins

Generous construction timeline with extension options

Sean + U.S. Bank vs. Typical Construction Lender

Most construction lenders require two closings, two sets of fees, and leave you managing the draw schedule yourself.

Three steps. One mortgage.

From blueprint to move-in day — Sean quarterbacks the financing so you can focus on the build.

Plan with Sean

Share your build plans, budget, and timeline. Sean structures a single-close loan that covers lot purchase (if needed), construction, and your permanent mortgage — all in one.

Build with Confidence

During construction, you pay interest-only on funds drawn. Sean manages the draw schedule with your builder, releasing funds at each milestone. Your permanent rate is already locked.

Move In with One Mortgage

When construction completes, your loan automatically converts to a permanent mortgage. No second closing. No re-qualification. No surprises. Just your new home.

Construction Loan FAQ

What's the difference between single-close and two-close construction loans?

What's the minimum project size?

Does renovation-to-permanent qualify?

How does the draw schedule work?

Can I combine this with a physician loan?

What's the typical timeline from application to breaking ground?

Can I include lot purchase in the construction loan?

Ready to plan your build?

90 seconds with Rosie to get your build budget. No credit impact. No obligation. Or book a 20-minute strategy call with Sean — free.

Construction Loans — Available in All 50 States

Sean is licensed nationwide. Select your state for local details.